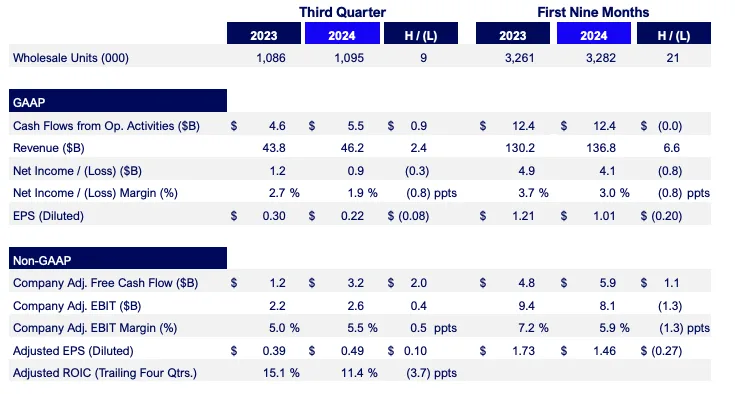

- Ford reports third quarter revenue of $46 billion; net income of $0.9 billion, including a previously announced $1 billion electric vehicle-related charge; adjusted EBIT of $2.6 billion

- Ford Pro revenue increases 13%; Ford Pro Intelligence paid software subscriptions up 30% to nearly 630,000 users

- Company declares fourth-quarter regular dividend of 15 cents per share

- Full-year 2024 adjusted EBIT now expected to be about $10 billion

Ford reported third-quarter 2024 results that indicate the long-term value creation made possible by a winning lineup of internal combustion, hybrid and electric vehicles for retail and commercial customers combined with an advantaged strategy and global footprint.

“We are in a strong position with Ford+ as our industry undergoes a sweeping transformation,” said Ford President and CEO Jim Farley. “We have made strategic decisions and taken the tough actions to create advantages for Ford versus the competition in key areas like Ford Pro, international operations, software and next-generation electric vehicles. Importantly, over time, we have significant financial upside as we bend the curve on cost and quality, a key focus of our team.”

Company Key Metrics Summary

Ford’s third-quarter revenue was $46 billion, up 5% from the same period a year ago. This marks the company’s 10th consecutive quarter of year-over-year revenue growth, benefits of a fresh and compelling product lineup that offers freedom of choice to both retail and commercial customers.

Company net income was $0.9 billion, down $0.3 billion from third-quarter 2023, due largely to a previously announced $1 billion electric vehicle-related charge that was part of actions taken to deliver a profitable, capital-efficient and growing electric vehicle business.

Adjusted earnings before interest and taxes, or EBIT, was $2.6 billion, a $352 million improvement year-over-year. The improvement was driven by higher volume and favorable mix, offset partially by electric vehicle pricing pressure and adverse exchange; overall costs were lower in the quarter.

“We are remaking the company with Ford+ into a higher-growth, higher-margin, more capital-efficient and more durable business,” said Ford Vice Chair and CFO John Lawler. “The work we have done over the past few years to restructure our global business — and tailor our product lineup to segments where we know our customers best — is driving continued growth and generating stronger and more consistent cash flow.”

Cash flow from operations in the third quarter was $5.5 billion, and adjusted free cash flow was $3.2 billion. At quarter-end, Ford had nearly $28 billion in cash and $46 billion in liquidity, providing considerable flexibility in a dynamic environment.

The company also declared a fourth-quarter regular dividend of 15 cents per share, payable on December 2 to shareholders of record at the close of business on November 7.

Business Segment Highlights

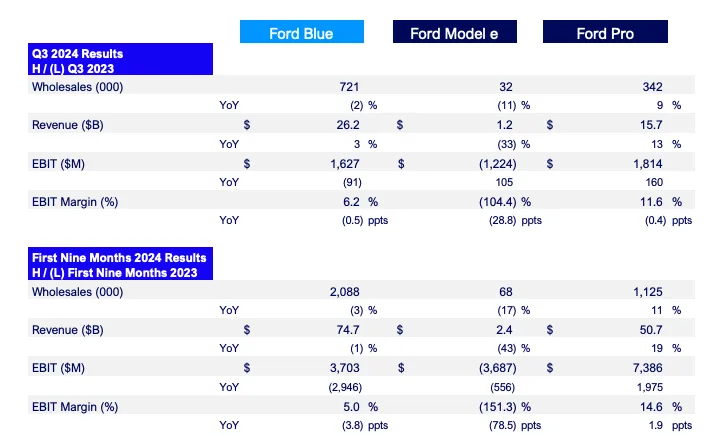

In the third quarter, Ford Pro generated $1.8 billion in EBIT – with a margin of 11.6% – on revenue of $15.7 billion, a 13% increase from the same period a year ago. The segment’s consistent delivery of year-over-year revenue growth has been fueled by a fresh product lineup and robust demand for Super Duty trucks and Transit vans.

Paid subscriptions to Ford Pro Intelligence were up 30% in the quarter to nearly 630,000 – and repair orders fulfilled by the company’s fleet of about 2,400 mobile service vehicles grew by 70%, underscoring the huge customer demand for digital and remote experiences.

Third-quarter revenue for Ford Blue was up 3% to $26.2 billion, despite a 2% decline in global wholesales due to discontinued low margin ICE passenger vehicles.

North America volume grew by 8% driven by newly launched trucks and SUVs that helped grow Ford’s market share in the U.S. during the quarter by 40 bps to 12.6%. Ford Blue EBIT of $1.6 billion and margin of 6.2% were both down year-over-year, due to adverse exchange and higher manufacturing costs, offset partially by lower warranty expense and higher net pricing.

Global hybrid vehicle sales increased 30% in the quarter, and the company’s hybrid mix remains on pace to approach 9% by year end, up over 2 points year-over-year, with more products on the way. Ford commanded 77% of the U.S. hybrid truck market during the quarter, with hybrid truck sales up 42% in the third quarter.

The quarter included strong truck sales as well as the launch of the all-new Ford Explorer and Lincoln Aviator in the U.S., with more refreshed and derivative products on the way, like the Maverick pickup and Bronco Sport SUV in Q4 and the new Expedition and Navigator in early 2025.

Ford Model e reported an EBIT loss of $1.2 billion. The $500 million of year-over-year cost improvements were offset by expected industrywide pricing pressure. The segment continues to improve its profit trajectory, achieving almost $1 billion in cost improvements year-to-date.

Ford continues to remove barriers to EV adoption by offering customers greater access to charging both at home, through the Ford Power Promise, and on the road through a growing charger network. And the nearly 3,000 Ford dealers now able to sell electric vehicles are a competitive advantage as Ford reaches new customers in areas of the U.S. that might otherwise be slow to adopt electric vehicles.

Ford Credit reported third-quarter earnings before taxes (EBT) of $544 million, an increase of $186 million year-over-year.

Full-Year 2024 Outlook

Ford now expects adjusted EBIT of about $10 billion with adjusted free cash flow between $7.5 billion and $8.5 billion. Capital expenditures are expected to be between $8 – $8.5 billion.

Full-year EBIT for Ford Pro is now expected to be about $9 billion, Ford Blue about $5 billion, and Model e a full-year loss of about $5 billion. Earnings before taxes from Ford Credit are now expected to be about $1.6 billion.

Ford plans to report fourth-quarter 2024 financial results following the close of market on Feb. 5, 2025.